How Can We

Help You?

Equity Specialty Services offers comprehensive support for investors dealing with Unrelated Business Income Tax (UBIT). Whether you need help preparing your Form 990-T, filing an extension for your IRA, or simply understanding the process, we’re here to assist. Choose the option that suits you best:

Watch to learn more about UBIT and how Equity Specialty Services can help with reporting:

Resources

Use the resources below to better understand this tax.

INVESTMENTS THAT COMMONLY TRIGGER UBTI

- Investments into leveraged funds and/or partnerships

- Investments into operating businesses structured as pass-through entities, like LLCs

- Debt-financed property

Example 1: Leveraged Funds

An IRA is a limited partner in an investment fund. The fund’s strategy uses leverage in addition to equity provided by its investor base.

Since the fund contains leveraging, UBTI may be reported on the annual K-1. If the UBTI reported exceeds $1,000, IRA partners in this scenario would need to file a 990-T.

For more information about this scenario, including where to look on a K-1 please refer to the Frequently Asked Questions below, or reach out to our team of specialists by emailing [email protected].

Example 2: Operating Business

If your IRA is invested in a passthrough entity such as an LLC or LP, and that entity operates a business, it may generate UBTI. An operating business is defined as a trade or business activity that is regularly carried on.

For example, if your IRA owns a restaurant, which operates as a regular business, the income generated from that restaurant would be considered UBTI for the IRA, and a 990-T would need to be prepared if the UBTI exceeds $1,000 for the tax year.

Example 3: Debt-Financed Property

An IRA owns an investment property. The property was acquired using a non-recourse loan. In this example, 55% of the property was purchased using the loan.

Annually, the net income attributable to the loan’s percentage ownership, in this case 55%, would be considered Unrelated Business Taxable Income (UBTI) which would be subject to Unrelated Debt-Financed Income, requiring a Form 990-T to be prepared and filed if the net income for the tax year exceeds $1,000.

Keep in mind that your IRA’s tax liability may fluctuate annually due to investment performance and other factors such as debt-to-equity ratio, so it’s important to monitor your investment regularly.

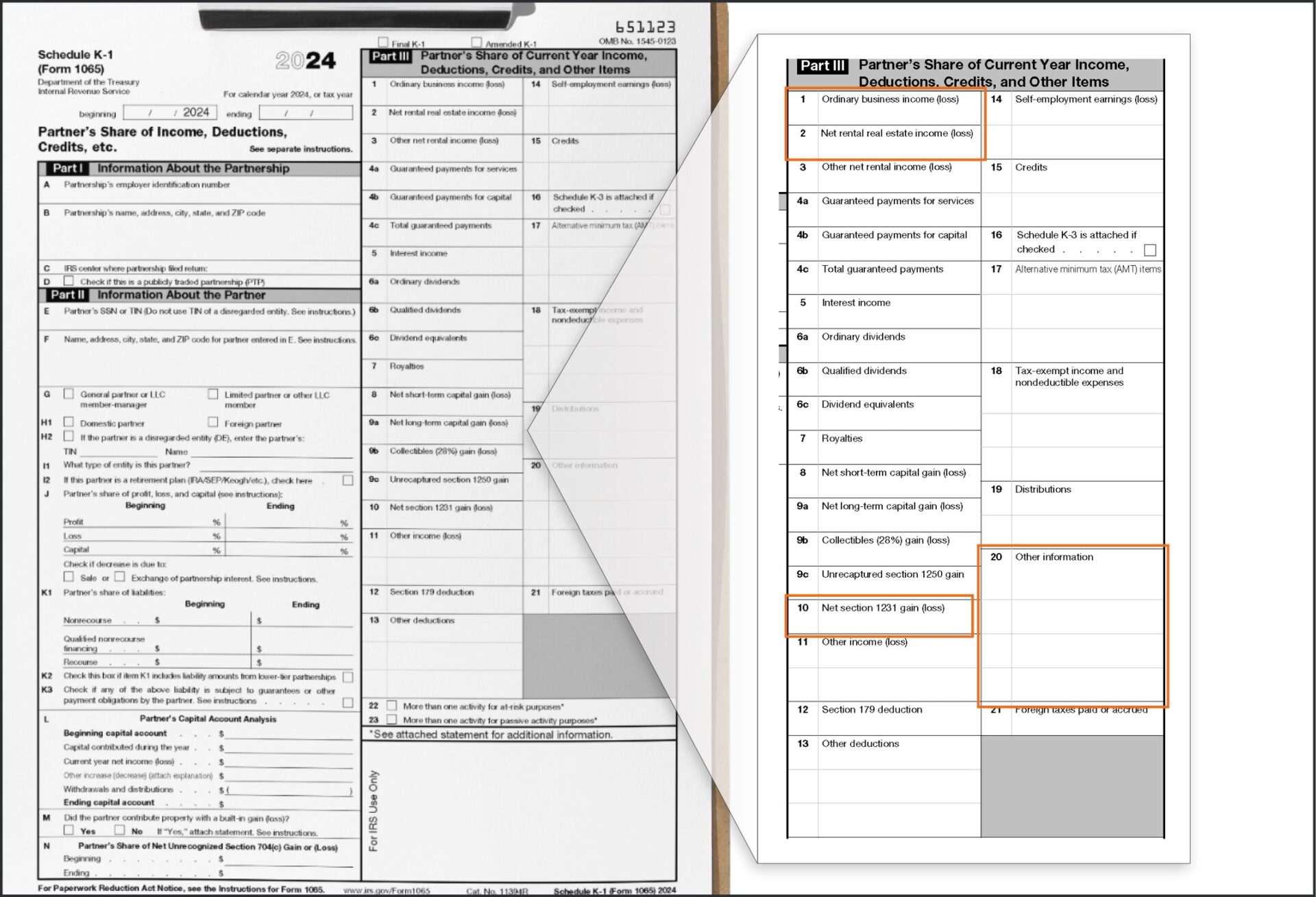

HOW CAN I DETERMINE IF MY INVESTMENT GENERATED UBTI?

While your tax advisor will be able to tell you for certain, indications of UBTI reported within an investment in a partnership, such as an LLC or LP, can be found on your annual K-1.

- If Box 20 contains code “V” UBTI was generated. If the amount of UBTI generated across the IRA exceeds $1,000 you must file a 990-T.

- If Box 20 does not contain a “V” but you show amounts, especially large amounts, in Box 1, Box 2, or in Box 10, it’s worth asking the K-1 issuer if any UBTI was generated in those figures.

- You can also check the K-1s supporting documentation to identify any references to Unrelated Business Taxable Income.

If you do not have your K-1 yet, let Equity help you file an extension for your IRA to provide more time to make your determination. Submit your request for an extension above.

For real estate investments without a K-1, calculating UBTI involves a few steps; here is a general outline:

- Determine your gross income. This is the total amount of income including rental, operational income.

- Calculate the debt-financed percentage. Determine the percentage of the property that is financed. This can be done by dividing the average debt by the averaged adjusted basis of the property during the year.

- Apply the debt-financed percentage to the income. Multiply the total income by the debt-financed percentage to find the attributable income that is subject to UBTI.

- Deduct related expenses. Subtract any expenses directly attributable to earnings of the debt-financed income. This includes interest, management fees, and other operational expenses.

- If your UBTI exceeds $1,000, report on Form 990-T.

As always, consult your tax advisor for additional information specific to your investments.

Additional Resources

How Equity Can Help

Equity’s specialized team is here for you! We offer the following services:

- Efficient preparation of 990-T forms

- Filing extensions for IRAs to provide additional time

- Assistance with determining whether UBTI was reported

To engage with our specialists, select how you would like to proceed above or send us a message at [email protected] and we will be in touch.

990-T Service Pricing

For 990-T pricing related to LLC/LP investments view our fee schedule here.

For 990-T pricing related to Debt-Financed real estate investments view our fee schedule here.

Frequently Asked Questions

What is Unrelated Business Income Tax (UBIT)?

What is Unrelated Debt-Financed Income (UDFI)?

Are UDFI and UBIT the same?

How can I determine if UBIT or UDFI applies to my investment?

What is defined as an operating business?

If I owe tax, how is that paid?

What are the current tax rates?

What if I don’t have my K-1 yet?

What are the key dates?

Why do I need to replace my IRA’s EIN?